College isn’t cheap — but borrowing more than you need could cost you far more than tuition.

Every year, millions of students sign up for private loans that seem safe on the surface: predictable, pre-approved, annual funding for school. But behind the scenes, many of those loans quietly create a mountain of unnecessary debt that could take decades to climb out of. Most borrowers don’t even realize they’ve fallen into the trap until it’s too late.

The Overborrowing Problem No One Warns You About

Private student loans typically force you to estimate all your education costs up front for the entire academic year and borrow a lump sum. Tuition, rent, books, food, fees — the works. But let’s be real: how accurately can you really predict what you’ll need six months from now?

So what happens? You round up. You borrow “just in case.” And when that extra money hits your bank account, it feels like security. But it’s not. It’s a balance that starts racking up interest from day one — even if you never spend it. And that “just in case” cushion adds up fast.

Repeat that for four years, compound the interest while deferring payments, and suddenly you’re thousands — sometimes tens of thousands — deeper in debt than you needed to be.

The Hidden Cost of Playing It Safe

Here’s the thing: borrowing more than you need might feel wise, but the numbers tell a different story. Let’s say you overborrow by $5,000 over the course of your degree. If you’re on a standard 10-year repayment plan at a 7.5% interest rate, that’s an extra $59 a month — or more than $7,100 in total payments for money you didn’t even use.

That’s a couple decades of Netflix. Or a trip to Thailand. Or a solid head start on retirement.

And beyond the dollars, there’s the stress. Higher balances mean bigger monthly payments, more interest, and more anxiety — especially for students trying to build a future while juggling job hunts, relocations, or grad school.

The Annual Loan Headache

There’s another catch to traditional private loans: you have to reapply every year.

Each year brings a new round of paperwork, credit checks, approvals, and uncertainty — right when you’re focused on exams, internships, or getting your life together. It’s exhausting, confusing, and for many families, downright overwhelming. So what’s the alternative?

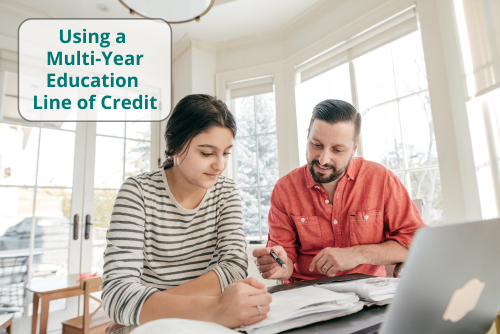

A Flexible Loan Model More Students Should Know About

Enter the student line of credit — a smarter, more flexible loan option offered by many credit unions.

Here’s how it works:

- You apply once, at the beginning of your college career.

- You’re approved for a total limit you can borrow from as needed each academic term.

- If your costs go down, or if you land a scholarship or a summer job, you borrow less.

- You only pay interest on the amount you actually use.

It’s a totally different mindset — one that aligns with how students actually live, spend, and adjust over time.

It’s like a student loan that finally respects your future self.

You stay in control. You borrow less. You save more.

Why Credit Unions Are Leading the Way

Credit unions aren’t in it for profit. They’re member-owned, community-rooted institutions that focus on financial well-being — not shareholder returns.

Organizations like Student Choice have helped bring this borrowing model to thousands of students since 2008. Their reusable line of credit is backed by hundreds of credit unions and gives borrowers access to funding across multiple years — with just one application.

That means:

- No reapplying and hard credit checks every year

- No interest on unused funds

- Longer repayment terms (up to 25 years)

- No penalties for paying it off early

- Fewer fees and more transparency

It’s not a gimmick. It’s just a better design.

From Loan Trap to Loan Hack

The line of credit model isn’t some flashy fintech breakthrough. It’s been here for years — but most students never hear about it because banks and private lenders dominate the high-cost marketing game.

That’s why it feels like a “loan hack.”

It’s a smarter, lesser-known option that works with your real life — not against it. More students (and parents) are starting to notice. Quietly, on campuses across the country, word is spreading: there’s a better way to borrow.

A Smarter Future Starts with Smarter Borrowing

Overborrowing doesn’t just delay graduation goals — it delays life. It means waiting longer to buy a house, start a business, or feel financially stable. But it doesn’t have to be that way. By borrowing only what you need — when you need it — you can:

- Avoid unnecessary debt

- Reduce stress and financial risk

- Make more accurate decisions, semester by semester

- Graduate with confidence, not regret

You don’t need to hack the system. You just need to stop borrowing more than you have to. Find your smarter student loan solution from a credit union today!